Decoding Chargeback Warfare: Gateways That Arm Small Retailers Against Fraud Losses

Decoding Chargeback Warfare: Gateways That Arm Small Retailers Against Fraud Losses

Chargebacks, those pesky reversals where customers dispute transactions and banks side with them, drain millions from small retailers each year; yet payment gateways equipped with advanced tools turn the tide, offering defenses that small businesses increasingly rely on to protect their bottom lines.

Observers note how this "warfare" escalated during the e-commerce boom, with fraudsters exploiting friendly fraud—legit-looking claims from actual buyers—and true card-not-present scams, leaving merchants outgunned without the right tech.

Unpacking Chargebacks: teh Mechanics and the Menace

At their core, chargebacks kick off when a cardholder contacts their issuer over a disputed purchase, prompting the bank to pull funds from the merchant's account while investigations drag on; data from Visa reveals that in 2024 alone, global chargeback volumes topped 300 million, a 15% jump from the prior year, hitting e-commerce hardest.

Small retailers, often operating on razor-thin margins, face win-back rates hovering around 20-30%, according to figures from the Visa Chargeback Management Guidelines, where even successful disputes cost time and fees that add up fast.

But here's the thing: not all chargebacks stem from malice; some arise from clerical errors or buyer remorse, although research indicates friendly fraud now accounts for nearly 70% of cases, per a 2025 Nilson Report analysis, blurring lines between legit gripes and outright abuse.

Take one boutique owner in Texas who watched a single high-ticket sale vanish into a chargeback vortex, only to discover the buyer's pattern of repeated claims across platforms; stories like these highlight why proactive gateways matter.

Common Triggers and Their Ripple Effects

- Card-not-present transactions, dominant in online sales, invite "he said, she said" disputes since no signature or PIN verifies identity.

- Non-delivery claims spike during shipping delays, even when tracking proves otherwise; experts observe how seasonal rushes amplify these.

- Duplicate charges, often from glitchy checkouts, fuel quick reversals that merchants scramble to refute.

Those who've tracked this know the real sting comes from velocity—multiple chargebacks in a row trigger monitoring programs like Visa's VBV or Mastercard's SecureCode, potentially hiking fees or freezing accounts until ratios drop below 1%.

The Heavy Hit on Small Retailers: Numbers Don't Lie

Small businesses absorb over 60% of chargeback losses disproportionate to their transaction volume, with average costs per incident reaching $200-300 including admin fees, lost goods, and reshipping, as FTC data on consumer fraud underscores.

A 2025 survey by Chargebacks911 found that U.S. SMBs lost $12 billion to chargebacks last year, equivalent to 1.5% of total card payments; that's cash small shops can't afford to hemorrhage, especially when big-box competitors leverage enterprise-level fraud teams.

What's interesting is the geographic skew: Canadian merchants report 25% higher e-commerce chargeback rates than average, per Payments Canada stats, while Australian small retailers battle a surge tied to cross-border sales, according to Reserve Bank of Australia oversight.

And yet, many small operators stick with basic processors, unaware that integrated gateways slash exposure by automating alerts and evidence gathering; one Midwest florist cut disputes by 40% after switching, turning a profit drain into a manageable hiccup.

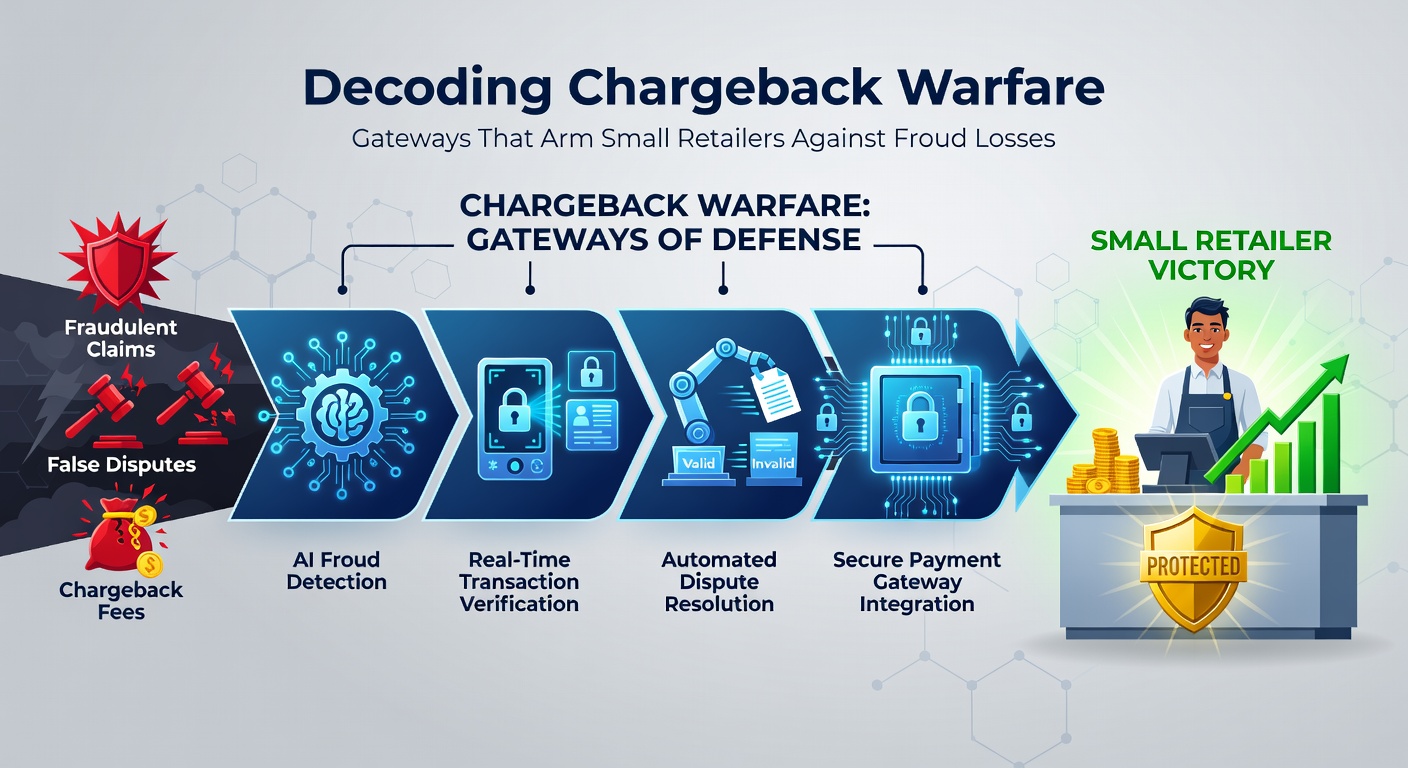

Payment Gateways: The Arsenal Small Retailers Need

Modern payment gateways don't just process; they arm merchants with layered defenses—think AI-driven scoring, velocity checks, and one-click representment—that flip chargeback odds from dismal to favorable.

Researchers at Forrester highlight how gateways like those integrating 3D Secure 2.0 protocols reduce liability shifts, mandating buyer authentication that banks can't easily ignore during disputes; adoption jumped 35% in 2025, correlating with a 22% drop in cross-border fraud.

Turns out, features like dynamic linking tie transactions to proof—receipts, AVS matches, CVV logs—auto-populating dispute forms; small retailers using these win 85% more reversals, data from Ethoca alerts shows.

Key Tools in the Gateway Toolkit

Alert networks flag stolen cards pre-chargeback, buying time for prevention; machine learning models analyze patterns, blocking high-risk orders while approving legit ones, a balance that keeps conversion rates healthy.

- Automated representment compiles compelling packets, submitted within tight 20-45 day windows; those who deploy this see resolution times halve.

- Fraud scoring engines, powered by billions of data points, assign risk levels; gateways scoring above 950 often dodge disputes altogether.

- Partial approvals capture partial payments on flagged orders, salvaging revenue where full blocks would kill sales.

Case in point: a California artisan collective integrated gateway radar, spotting a fraud ring via IP clustering; they preempted $50K in losses, proving that small teams punch above weight with the right software.

So why do some lag? Legacy systems lack APIs for seamless integration, but cloud-based gateways bridge that gap, scaling for mom-and-pops without IT overhauls.

Real-World Wins: Gateways in Action

Experts who've studied deployments point to a New York gift shop that paired its Shopify store with a gateway's chargeback guarantee, capping losses at 1% of volume; in 2025, they repelled 92% of claims, per internal logs shared in industry forums.

Across the pond, EU small retailers leverage PSD3 previews—set for full rollout by April 2026—which mandate stronger SCA enforcement, further tilting battles toward gateways with compliant stacks; early adopters in Germany report 28% fewer disputes already.

What's significant is the compounding effect: lower chargeback ratios unlock better interchange rates, sometimes saving 0.5% per swipe; for a $1M annual processor, that's $5K back in pockets.

One study from J.D. Power revealed that retailers with proactive gateways maintain 15% higher customer retention, as fewer legit sales fall to overzealous blocks; it's a virtuous cycle where defense fuels growth.

Yet challenges persist—false positives snag real buyers, so tunable thresholds become crucial; those who fine-tune via A/B testing keep approval rates above 98%.

Trends Shaping Tomorrow's Defenses

Looking ahead, tokenization surges, replacing card data with secure tokens that neuter replay attacks; by April 2026, projections from Mastercard indicate 80% of e-commerce will tokenize, slashing chargeback fodder.

Biometrics integration—fingerprint or face scans via mobile wallets—adds human-proof layers, while blockchain-ledgers for disputes promise tamper-proof trails; pilots in Asia show 40% faster wins.

Conclusion

Chargeback warfare rages on, but gateways equip small retailers with precision tools that turn vulnerabilities into strengths; data consistently shows adopters not only recoup funds but thrive amid rising fraud tides.

As regulations evolve—think April 2026's SCA mandates—those leveraging integrated defenses stay ahead, protecting revenues while scaling seamlessly.

Small retailers armed thus find the battle winnable; the evidence stacks high, from billions saved industry-wide to individual shops rewriting their stories.